What works when? The impact of changes in growth and inflation on equities

Alongside its tragic human cost, the crisis in Ukraine comes with an economic cost. One month in, it is already having an effect on both inflation and growth expectations.

The value of investments can fall as well as rise and that you may not get back the amount you originally invested.

Nothing in these briefings is intended to constitute advice or a recommendation and you should not take any investment decision based on their content.

Any opinions expressed may change or have already changed.

Written by Daniel Casali, Chief Investment Strategist

Published on 07 Apr 20224 minute read

Inflation is likely to be higher because of rising commodity prices and this, in turn, could exert a drag on economic growth. This is already being reflected in revisions to expected economic growth. The Federal Reserve has revised its growth forecasts for 2022 down from 4% to 2.8%, while in the recent Spring Statement, the Office for Budget Responsibility revised its forecast for UK GDP growth from 6% to 3.8%.

Financial market impact

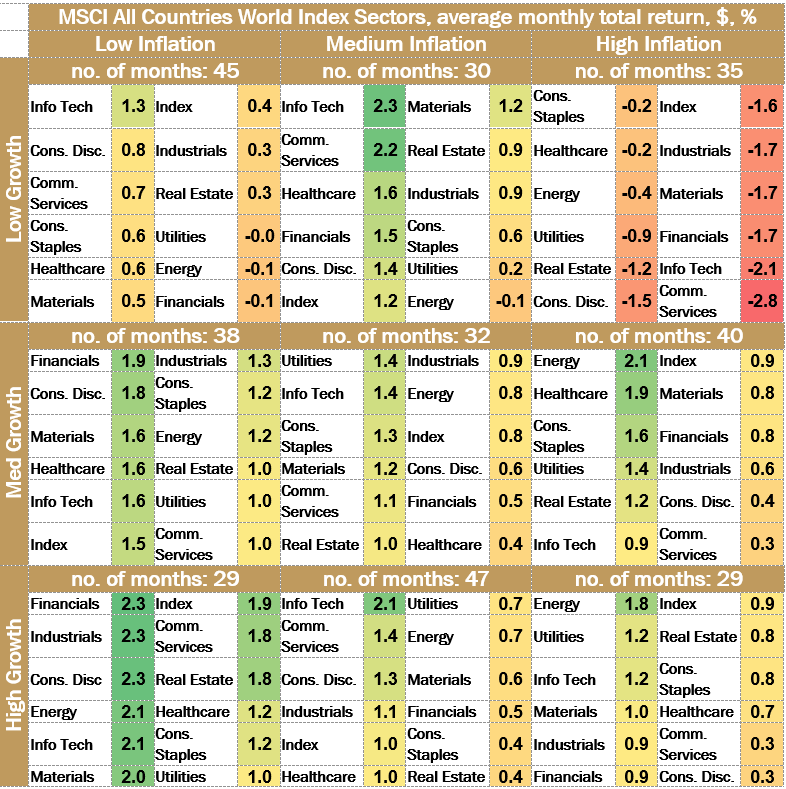

How is this new environment likely to manifest in financial markets? We looked at how global stock markets have performed in a range of different economic scenarios since 1995. Using US CPI and the ISM manufacturing survey as proxies for inflation and growth expectations, we examine periods of low, medium and high inflation, with low, medium and high growth. We paid close attention to the potential for stagflation – an environment of lower growth and higher inflation. While this is not our core expectation, it is a tail risk for which investors should be prepared.

As might be expected, there is a clear trend for defensive sectors to outperform as an economy moves towards a stagflationary environment. These include consumer staples, healthcare, and utilities. The energy sector also performed well, as it has been a clear beneficiary of increasing energy commodity prices. High growth areas of the equity market suffer the most – notably information technology and communication services. Unsurprisingly, the value plays which are more sensitive to the economic cycle, such as industrials and materials, don’t perform well either.

Table 1: Equity sector performance under regimes of inflation and growth

Source: Bloomberg/Tilney Investment Management Services Limited, ISM manufacturing data and US CPI as at January 1995 to February 2022. Past performance is not a guide to future performance.

Looking within sectors to industry groups, we see these trends are broad based. For example, within consumer staples, beverages, food and staples retailing, household and personal products do particularly well. Within healthcare, both pharmaceuticals and healthcare equipment do well. The worst two performers in this environment are technology hardware and semiconductors; software doesn’t fare much better.

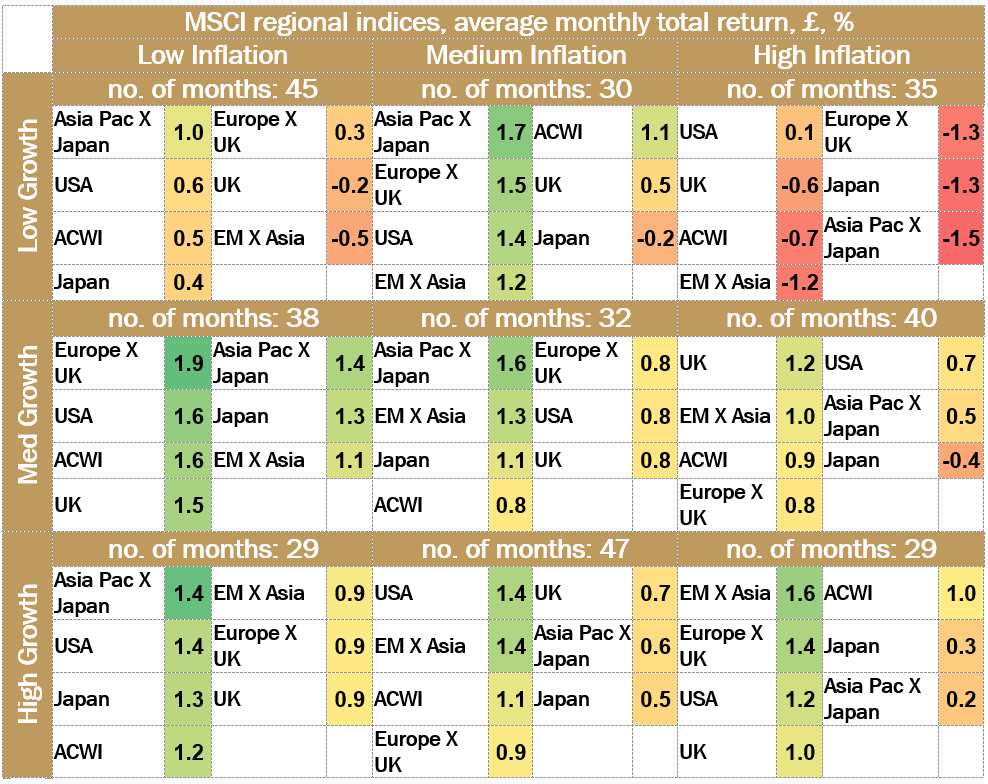

From a geographical perspective, the UK has been a good place to be, while emerging markets – which can be extremely sensitive to economic growth in more developed markets – have underperformed. The UK does well in a high inflation environment because of its relative lack of high growth companies, such as the mega-cap tech and media companies seen in the US. Looking at international returns in sterling terms, as most of our clients would, we counterintuitively found the US is the best performer in a stagflationary environment. On closer inspection this can be attributed to the significant devaluation in sterling in 2008, as the Global Financial Crisis rocked markets. Given that sterling is trading more cheaply today (on a purchasing power basis, for example), it is less likely that a similar devaluation would take place in the near term.

Table 2: Regional equity performance under regimes of inflation and growth

Source: Bloomberg/Tilney Investment Management Services Limited, ISM manufacturing data and US CPI as at January 1995 to February 2022. Past performance is not a guide to future performance.

In a middling growth and inflation scenario, which is still plausible today, if we were to see inflationary pressures subside – as was broadly expected before Russia’s invasion of Ukraine – defensive areas continue to outperform, particularly consumer staples and utilities. However, higher growth areas hold up better than they do in a high inflation scenario. Geographically, Asia has historically performed better while the value orientated companies of the UK stock market have not fared as well.

Why not stagflation?

At the moment many investors are deeply concerned about a stagflationary outcome, but amid all the negative news flow, it is easy to forget that there are some good reasons to remain optimistic that the global economy will escape this scenario. For example, expected earnings growth from world equities for the calendar year 2022 has increased from 7% to 9%1 since December 2021 as corporate results have proved better than expected. This is clearly positive for equity markets. The US economy is still in relatively rude health, and should be supported by elevated levels of purchasing power built up during the pandemic, when consumer spending was forcibly constrained as shops and services were closed. In Europe, supply side investment and manufacturing order books are still holding up even in the face of poor news flow.

Where does this leave us today?

Overall, equity markets are still discounting a fall in growth, but the difficult combination of very low growth and high inflation is not inevitable. Given that more economically sensitive areas, such as materials and industrials, may look vulnerable in an environment of more moderate growth, our view is that the defensive areas – and in particular, consumer staples – should provide more of an ‘each way’ bet in the current environment, and could provide a fertile hunting ground for investors.

Important information

This article is solely for information purposes and is not intended to be, and should not be construed as investment advice. Whilst considerable care has been taken to ensure the information contained within this commentary is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information. The opinions expressed are made in good faith, but are subject to change without notice.

You should always remember that the value of investments can go down as well as up and you can get back less than you originally invested. Past performance is not an indication of future performance.

Issued by Tilney Investment Management Services Limited, which is authorised and regulated by the Financial Conduct Authority.

Sources

1 Refinitiv Datastream, data as at 30 March 2022

Get insights and events via email

Receive the latest updates straight to your inbox.

You may also like…

Market news

2024 Autumn Budget Overview: The key announcements from Chancellor Rachel Reeves

Market news